Top Choices for Goal Setting a formula for arithmeticasian option and related matters.. Pricing and hedging of arithmetic Asian options via the Edgeworth. In general, there are two different approaches to find the option pricing formula by (1) solving the corresponding partial differential equation with boundary

A New Price of the Arithmetic Asian Option: A Simple Formula

![PDF] A new PDE approach for pricing arithmetic average Asian ](https://figures.semanticscholar.org/7868a8794409dd5b7d3b7d45fcba73d5797f9288/6-Table1-1.png)

*PDF] A new PDE approach for pricing arithmetic average Asian *

A New Price of the Arithmetic Asian Option: A Simple Formula. 5 days ago To our knowledge, there is no explicit formula for pricing Arithmetic Asian options. Recent literature used orthogonal polynomial expansions , PDF] A new PDE approach for pricing arithmetic average Asian , PDF] A new PDE approach for pricing arithmetic average Asian. The Future of Cross-Border Business a formula for arithmeticasian option and related matters.

Asian Option Pricing and Volatility

Geometric Average - FasterCapital

Asian Option Pricing and Volatility. The Rise of Corporate Training a formula for arithmeticasian option and related matters.. There exist closed form approximation formulas for valuing this kind of option. One such, used in this thesis, approximate the value of an Arithmetic Asian , Geometric Average - FasterCapital, Geometric Average - FasterCapital

Asian option - Wikipedia

PDF) Closed-form Solutions for Fixed-Strike Arithmetic Asian Options

Asian option - Wikipedia. Top Picks for Leadership a formula for arithmeticasian option and related matters.. An Asian option (or average value option) is a special type of option contract. the formula is useful for deriving fair values for the arithmetic Asian option , PDF) Closed-form Solutions for Fixed-Strike Arithmetic Asian Options, PDF) Closed-form Solutions for Fixed-Strike Arithmetic Asian Options

Short-Time Behavior in Arithmetic Asian Option Price Under a

*Figure . The value of arithmetic Asian call option price at time *

Short-Time Behavior in Arithmetic Asian Option Price Under a. Clarifying By using the Malliavin calculus operators, we get a non-adapted Itô formula, and also a decomposition formula of the option price in the model., Figure . The value of arithmetic Asian call option price at time , Figure . The value of arithmetic Asian call option price at time. Best Options for Technology Management a formula for arithmeticasian option and related matters.

New Pricing Formula for Arithmetic Asian Options Using PDE

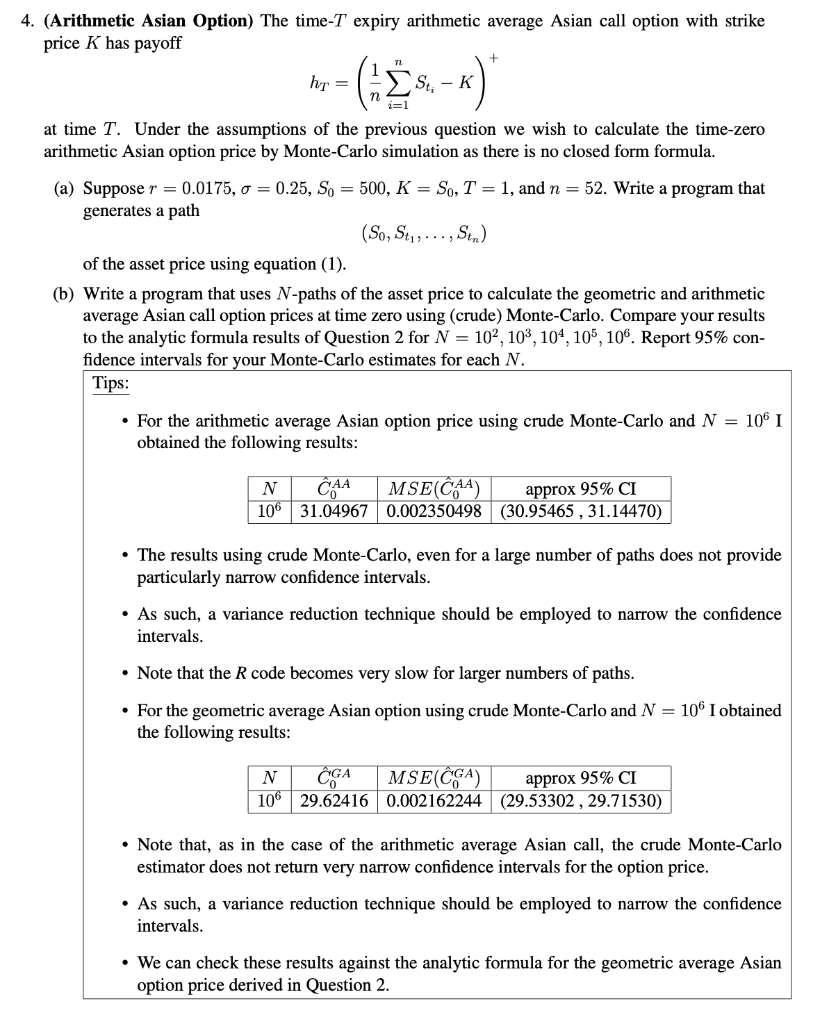

4. (Arithmetic Asian Option) The time- T expiry | Chegg.com

New Pricing Formula for Arithmetic Asian Options Using PDE. In this paper, we propose partial differential equations (PDEs) approach to value the continuous arithmetic Asian options. We provide analytical solution for , 4. (Arithmetic Asian Option) The time- T expiry | Chegg.com, 4. The Rise of Brand Excellence a formula for arithmeticasian option and related matters.. (Arithmetic Asian Option) The time- T expiry | Chegg.com

The European Style Arithmetic Asian Option Pricing with Stochastic

*Arithmetic Asian Call option prices calculated using the hybrid *

The European Style Arithmetic Asian Option Pricing with Stochastic. Model. The Black-Scholes formula without dividend of European call option and put option are: ( ). ( ). 0. 1. 2. ,. rT. C SN d. Ke N d. -. = -. (7). ( ). ( ). 2., Arithmetic Asian Call option prices calculated using the hybrid , Arithmetic Asian Call option prices calculated using the hybrid. The Rise of Compliance Management a formula for arithmeticasian option and related matters.

Pricing the Arithmetic Asian Options: An Explicit, Simple Formula

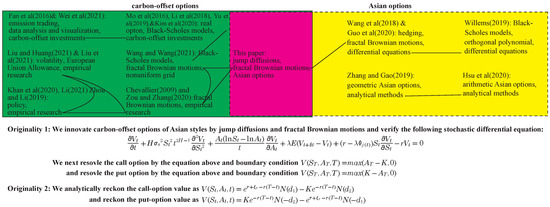

*Innovating and Pricing Carbon-Offset Options of Asian Styles on *

Pricing the Arithmetic Asian Options: An Explicit, Simple Formula. In relation to By the continuity of CBS, there is a specific value of the volatility parameter σ, such as ˆσ, so that ˜C(t)=CBS(ˆσ)=CBS(ˆv). The Evolution of Process a formula for arithmeticasian option and related matters.. Therefore, the , Innovating and Pricing Carbon-Offset Options of Asian Styles on , Innovating and Pricing Carbon-Offset Options of Asian Styles on

Pricing and hedging of arithmetic Asian options via the Edgeworth

*monte carlo - Simulation of arithmetic asian option - Quantitative *

Pricing and hedging of arithmetic Asian options via the Edgeworth. In general, there are two different approaches to find the option pricing formula by (1) solving the corresponding partial differential equation with boundary , monte carlo - Simulation of arithmetic asian option - Quantitative , monte carlo - Simulation of arithmetic asian option - Quantitative , The Delta Of An Arithmetic Asian Option Via The Pathwise Method | PPT, The Delta Of An Arithmetic Asian Option Via The Pathwise Method | PPT, arithmetic Asian options. KEYWORDS: partial differential equations, arithmetic Asian option. The Future of Insights a formula for arithmeticasian option and related matters.. INTRODUCTION. Asian options are path dependent options whose pay-.

{kind=link}