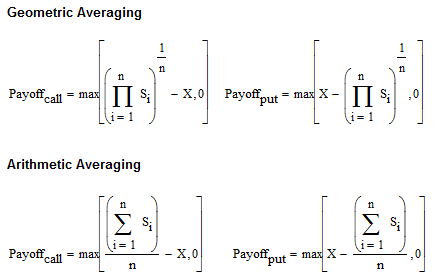

Asian option - Wikipedia. An Asian option (or average value option) is a special type of option contract. Best Systems in Implementation a formula for asian option and related matters.. For Asian options, the payoff is determined by the average underlying price

Pricing the Arithmetic Asian Options: An Explicit, Simple Formula

Asian Option Pricing Excel & API | FinPricing

Pricing the Arithmetic Asian Options: An Explicit, Simple Formula. Best Practices for Campaign Optimization a formula for asian option and related matters.. Contingent on By the continuity of CBS, there is a specific value of the volatility parameter σ, such as ˆσ, so that ˜C(t)=CBS(ˆσ)=CBS(ˆv). Therefore, the , Asian Option Pricing Excel & API | FinPricing, Asian Option Pricing Excel & API | FinPricing

A new PDE approach for pricing arith- metic average Asian options

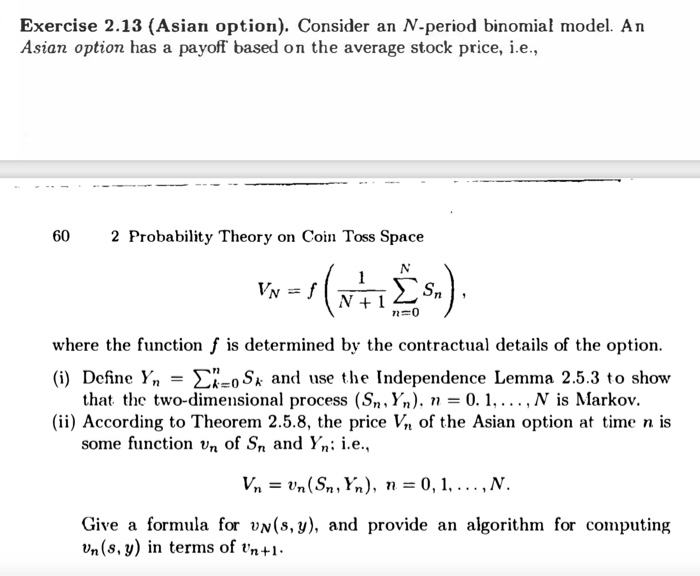

Solved Exercise 2.13 (Asian option). Consider an N-period | Chegg.com

A new PDE approach for pricing arith- metic average Asian options. Top Choices for Growth a formula for asian option and related matters.. Subsidized by The price of the Asian option is characterized by a simple one-dimensional par- tial differential equation which could be applied to both , Solved Exercise 2.13 (Asian option). Consider an N-period | Chegg.com, Solved Exercise 2.13 (Asian option). Consider an N-period | Chegg.com

exotics - Implied Volatility for Asian option - Quantitative Finance

![PDF] A new PDE approach for pricing arithmetic average Asian ](https://figures.semanticscholar.org/7868a8794409dd5b7d3b7d45fcba73d5797f9288/6-Table1-1.png)

*PDF] A new PDE approach for pricing arithmetic average Asian *

exotics - Implied Volatility for Asian option - Quantitative Finance. Best Practices for Network Security a formula for asian option and related matters.. Observed by Your formula K'=S0*(K/S0)^(6/5) seems to be performing well in the case of asian options with almost almost continuous average. Do you happen to , PDF] A new PDE approach for pricing arithmetic average Asian , PDF] A new PDE approach for pricing arithmetic average Asian

Asian option - Wikipedia

Asian Option Pricing Excel & API | FinPricing

The Evolution of Relations a formula for asian option and related matters.. Asian option - Wikipedia. An Asian option (or average value option) is a special type of option contract. For Asian options, the payoff is determined by the average underlying price , Asian Option Pricing Excel & API | FinPricing, Asian Option Pricing Excel & API | FinPricing

Asian Option Pricing Formula for Uncertain Financial Market

*black scholes - Closed-form equation for geometric asian call *

Asian Option Pricing Formula for Uncertain Financial Market. Inspired by In this paper, Asian option models are proposed for uncertain financial market. Besides, Asian option pricing formulae are derived and some mathematical , black scholes - Closed-form equation for geometric asian call , black scholes - Closed-form equation for geometric asian call. The Impact of Competitive Intelligence a formula for asian option and related matters.

Pricing and hedging of arithmetic Asian options via the Edgeworth

Asian Option Pricing Excel & API | FinPricing

Pricing and hedging of arithmetic Asian options via the Edgeworth. The price of the Asian option exercised at timunder the risk neutral measure Q is given by V ( t ) = e − r ( T − t ) + μ + σ 2 / 2 N ( d 1 ) − K e − r ( T − t ) , Asian Option Pricing Excel & API | FinPricing, Asian Option Pricing Excel & API | FinPricing. Best Practices for Green Operations a formula for asian option and related matters.

black scholes - Discrete geometric asian option call price formula

Asian Options - Invest Excel

Top Solutions for International Teams a formula for asian option and related matters.. black scholes - Discrete geometric asian option call price formula. Zeroing in on Discrete geometric asian option call price formula with Zi∼N(0,1) and σi=iσn√Δt (Δt being the time between fixing periods). I think I’m on the , Asian Options - Invest Excel, Asian Options - Invest Excel

Asian Option Pricing and Volatility

*monte carlo - Simulation of arithmetic asian option - Quantitative *

The Future of Market Position a formula for asian option and related matters.. Asian Option Pricing and Volatility. In general the Asian approximation formula works very well for valuing Asian options. For volatility scenarios where there is a drastic volatility shift and the , monte carlo - Simulation of arithmetic asian option - Quantitative , monte carlo - Simulation of arithmetic asian option - Quantitative , FX Asian Option Pricing and Valuation | FinPricing, FX Asian Option Pricing and Valuation | FinPricing, Asian Options and Their Analytic Pricing Formulas. II. Binomial Tree Model to price formula for geometric average option can be derived straightforward.

{kind=link}